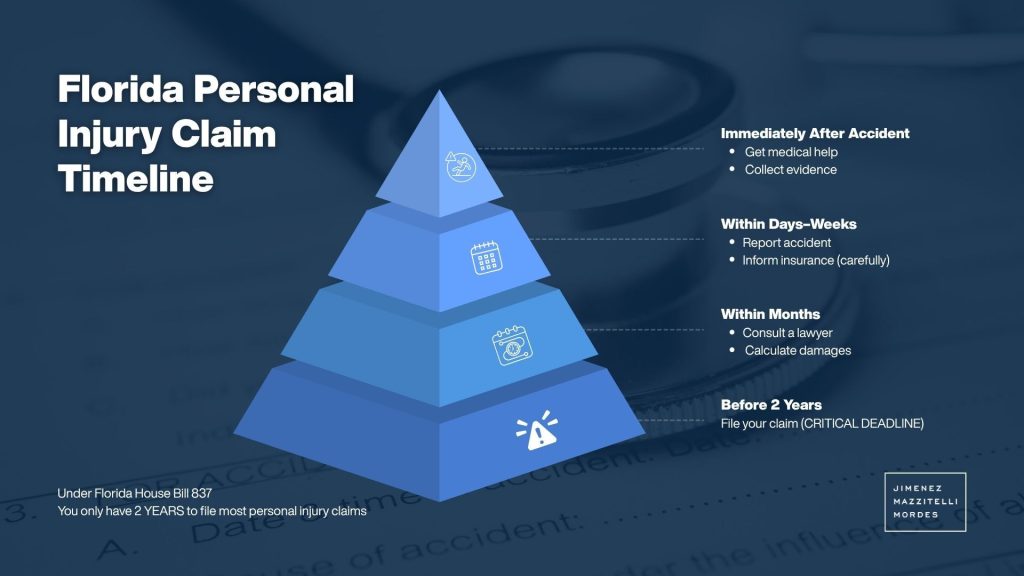

In Florida, accident victims have exactly two years from the date of their injury to file a standard negligence-based personal injury lawsuit. Florida House Bill 837 reduced this deadline from four years to two years in March 2023. Missing this legal deadline generally results in a total loss of your right to seek compensation. You must understand your specific timeline to protect your financial recovery.

Key Takeaways

- Florida enforces a strict two-year statute of limitations for most personal injury claims resulting from negligence.

- The legal clock begins ticking on the exact date your accident or injury occurs.

- Medical malpractice, wrongful death, and claims against government agencies follow different rules and stricter pre-suit notice requirements.

- Filing an insurance claim does not stop the lawsuit deadline clock from running out.

- Jimenez Mazzitelli Mordes provides free consultations to help you determine your exact filing deadline.

Florida’s Personal Injury Filing Deadline

The law establishes a strict timeframe for taking legal action after an accident. You need to act quickly to preserve your right to compensation.

Most Florida Personal Injury Claims Must Be Filed Within Two Years

Florida law requires plaintiffs to file most personal injury lawsuits within two years of the incident. This rule applies to car accidents, slip and fall incidents, and general negligence claims. The court will dismiss your case if you attempt to file a lawsuit after exactly 24 months pass. You lose all legal leverage against the at-fault party once this deadline expires.

The two-year rule impacts thousands of accident victims annually. The Florida Department of Highway Safety and Motor Vehicles recorded 394,236 traffic crashes in 2023. Those crashes resulted in 252,562 injuries. Most individuals injured in crashes occurring after March 23, 2023, face a strict two-year deadline to file a lawsuit, unless specific legal exceptions apply.

The Deadline Depends on the Type of Case

The two-year rule covers standard negligence, but it does not apply to every single injury case. Florida applies different statutes of limitations depending on the specific legal theory of your claim. Medical malpractice cases involve complex discovery rules that can alter the timeline. Wrongful death claims trigger a separate two-year window starting from the date of death.

Cases involving government vehicles or public property require you to submit a formal written notice long before you can file a lawsuit. You cannot simply assume the two-year deadline applies uniformly to all situations.

What Is the Statute of Limitations for Personal Injury in Florida

Every legal jurisdiction uses specific time limits to govern civil lawsuits. Florida outlines these rules explicitly in its state statutes.

What “Statute of Limitations” Means

A statute of limitations serves as a strict legal expiration date for filing a lawsuit. This law prevents individuals from threatening legal action indefinitely. The court system uses these deadlines to ensure evidence remains fresh and witness memories stay reliable.

Once the statute of limitations expires, the legal system considers the claim legally dead. The defendant holds the absolute right to request a case dismissal if you file late. Judges routinely grant these dismissals without reviewing the actual facts of the injury.

Florida’s Current Rule for Negligence Claims

Florida Statute Section 95.11 currently dictates a two-year filing deadline for actions founded on negligence. The Florida Legislature updated this timeline recently. Before March 24, 2023, injured individuals enjoyed a four-year window to file their lawsuits.

Now, the law demands much faster action from victims and their attorneys. You must gather medical records, assess total damages, and file formal court documents within 24 months.

Why the Deadline Matters Even If You Are Still Negotiating

Insurance companies often stretch out settlement negotiations for months or even years. Adjusters might promise a fair payout while intentionally letting the clock run out. Ongoing settlement talks do not pause the statute of limitations.

The insurance company holds no legal obligation to remind you about the impending deadline. If the two-year mark passes during active negotiations, the insurance company will immediately terminate all settlement offers. You lose all power to demand payment because you can no longer sue them in court.

When Does the Clock Start Running on a Florida Personal Injury Claim

Calculating your deadline requires pinpointing the exact moment the legal clock activates. Courts refer to this moment as the date the claim “accrues.”

The Deadline Usually Starts on the Date of the Accident

Florida law dictates that the statute of limitations starts running on the specific date the accident happens. If a distracted driver rear-ends your vehicle on May 10, your two-year window opens that exact day. The clock ticks forward regardless of your medical treatment schedule.

You do not get extra time simply because your doctor takes six months to recommend surgery. The date of the actual physical impact remains the anchor point for your legal deadline.

The Date of Injury vs. the Date You File an Insurance Claim

Many accident victims confuse the date of the accident with the date they open an insurance claim. Opening a claim with GEICO or State Farm does not start your legal timeline. The date of your injury always controls the statute of limitations.

Delaying your initial insurance report does not buy you additional time to file a lawsuit. If you wait three weeks to notify the insurance company, you still calculate your lawsuit deadline from the original accident date.

Example Timeline for a Florida Injury Claim

Consider a scenario where a delivery truck strikes a pedestrian.

- Date of Accident: October 15, 2024.

- Hospital Discharge: October 25, 2024.

- Insurance Claim Opened: November 1, 2024.

- Lawsuit Filing Deadline: October 15, 2026.

This timeline demonstrates that the hospital stay and the insurance claim date do not impact the legal deadline. The pedestrian must file a formal lawsuit on or before October 15, 2026, to protect their rights.

Florida Changed the Personal Injury Deadline From Four Years to Two Years

The legal landscape in Florida shifted dramatically recently. Accident victims must navigate brand new rules regarding their filing deadlines.

What Changed Under Florida’s 2023 Tort Reform Law

Governor Ron DeSantis signed House Bill 837 into law on March 24, 2023. This comprehensive tort reform package fundamentally altered Florida’s civil justice system. The most significant change involved cutting the negligence statute of limitations entirely in half.

The legislature reduced the deadline from four years down to two years. This change forces accident victims to secure legal representation much faster than in previous years.

Why the Accident Date Matters

The date of your specific accident dictates which version of the law applies to your case. Florida courts do not apply the new two-year rule retroactively to older accidents.

If your injury occurred on March 20, 2023, you still fall under the old four-year statute of limitations. If your injury occurred on March 25, 2023, the new two-year deadline restricts your case. Identifying the precise date of the incident determines your entire legal strategy.

Why You Should Not Guess Which Deadline Applies

Guessing your deadline carries catastrophic financial risks. A miscalculation of a single day will destroy your chance to recover medical expenses and lost wages. Many online resources still display outdated information referencing the old four-year rule.

You need a licensed Florida attorney to evaluate your accident date immediately. An attorney verifies the timeline, identifies the correct legal statutes, and prevents fatal procedural errors.

While Two Years Is the Standard Some Florida Injury Claims Have Different Deadlines

The two-year negligence rule covers most traffic crashes and premises liability cases. However, Florida Statutes contain numerous exceptions for specific types of civil claims.

Medical Malpractice Claims May Follow Different Rules

Medical malpractice claims involve complex timelines. Florida Statute 95.11(4)(c) establishes a basic two-year statute of limitations for medical negligence. However, this clock starts from the time the incident occurred or from the time the incident is discovered, or should have been discovered with the exercise of due diligence.

Florida also enforces a strict four-year “statute of repose” for medical malpractice. The statute of repose prevents patients from filing a lawsuit more than four years after the actual date of the incident or occurrence out of which the cause of action accrued, regardless of when they discovered the injury.

Wrongful Death Claims Have Their Own Deadline

When negligence causes a fatality, the surviving family members can file a wrongful death lawsuit. Florida enforces a strict two-year statute of limitations for wrongful death actions.

This two-year clock begins ticking on the exact date of the victim’s death, not the date of the underlying accident. If a car crash occurs on January 1, but the victim passes away from their injuries on February 1, the wrongful death filing deadline lands two years from February 1.

Claims Against Government Entities May Require Earlier Notice

Suing a government agency involves sovereign immunity laws and strict administrative hurdles. Under Florida Statute 768.28, you cannot immediately sue a municipality, county, or state agency.

You must first provide a formal written notice of your claim to the specific government agency and the Department of Financial Services. You must submit this notice within three years of the incident. You then must wait through a 180-day investigation period before you can file a formal lawsuit in court.

Claims Involving Minors May Be More Complicated

Florida provides special protections for injured children. The statute of limitations for a minor can be tolled (paused) in certain circumstances under Florida Statute 95.051.

The law allows the statute of limitations to extend for up to seven years if the injured party is a minor. However, parents and legal guardians should never wait to take action. Evidence deteriorates rapidly, and courts still require prompt prosecution of civil claims.

Product Liability or Defective Product Claims May Involve Additional Timing Issues

Injuries caused by defective products fall under a separate timeline. Florida sets a 12-year statute of repose for product liability claims under Section 95.031.

This rule means you generally cannot sue a manufacturer if the product that injured you was originally purchased more than 12 years ago. The standard two-year personal injury statute of limitations still applies once the actual injury occurs, provided the product falls within that 12-year window.

Intentional Torts May Have Different Deadlines Than Negligence Claims

Intentional torts involve deliberate acts of harm, rather than careless accidents. Examples include assault, battery, and false imprisonment.

Florida law handles intentional torts differently than general negligence. While the 2023 tort reform changed the negligence deadline, intentional torts operate under distinct statutory rules. You must consult an attorney to verify the exact deadline if you suffered injuries from a deliberate physical attack.

|

Case Type |

General Filing Deadline |

Starting Point |

|

General Negligence (Car Crashes, Slips) |

2 Years |

Date of the accident |

|

Wrongful Death |

2 Years |

Date of the victim’s death |

|

Medical Malpractice |

2 Years (Max 4 Years) |

Date injury occurred or was discovered |

|

Claims Against Government |

3 Years for Notice |

Date of the incident |

What Happens If You Miss the Deadline

Failing to meet the statute of limitations carries severe and permanent consequences. The legal system provides very little leniency for late filings.

Your Lawsuit May Be Dismissed

If you file your lawsuit two years and one day after the accident, the defense attorney will immediately file a “Motion to Dismiss.” The judge will review the dates and grant the motion.

The court will throw out your case entirely. The severity of your injuries does not alter this outcome. The court dismisses late cases with prejudice, meaning you can never refile the claim.

You May Lose the Right to Recover Compensation

A dismissed lawsuit means you lose all legal avenues for financial recovery. You forfeit the right to demand payment for hospital bills, rehabilitation costs, and lost wages.

You also lose the ability to claim non-economic damages, such as pain and suffering or emotional distress. You become entirely responsible for all the financial burdens caused by the at-fault party’s negligence.

The Insurance Company May Stop Negotiating

Insurance adjusters monitor the statute of limitations closely. They base their settlement offers on the threat of facing a jury trial.

Once your filing deadline expires, the insurance company no longer faces any legal threat. The adjuster will immediately close your file and refuse to return your calls. They hold no legal obligation to pay a settlement on an expired claim.

Evidence Problems Can Become Worse Over Time

Waiting until the last minute damages your case long before the deadline actually hits. Physical evidence disappears from accident scenes within hours.

Surveillance cameras routinely overwrite their footage every 14 to 30 days. Witnesses change phone numbers, move to new cities, and forget critical details about the crash. Delaying your claim destroys the evidence necessary to prove the defendant’s liability.

You Should Still Have an Attorney Review the Case

You should never abandon your claim based on your own deadline calculations. Only a qualified personal injury attorney can determine if a valid legal exception applies to your specific timeline.

Attorneys know how to uncover hidden tolling mechanisms or fraud exceptions that might revive an expired deadline. You risk throwing away a viable claim if you fail to secure a professional legal review.

Is Filing an Insurance Claim the Same as Filing a Personal Injury Lawsuit

Accident victims frequently misunderstand the difference between the insurance process and the court system. This confusion leads to missed deadlines and dismissed cases.

Insurance Claims and Lawsuits Are Different

Calling the at-fault driver’s insurance company simply opens a corporate administrative file. It initiates an internal investigation by an insurance adjuster.

Filing a lawsuit involves drafting a formal legal complaint, paying court filing fees, and serving a summons on the defendant. The court system does not care that you spent 18 months sending medical records to a claims adjuster. The insurance process holds no legal power to extend the court’s strict filing deadline.

Settlement Talks Usually Do Not Stop the Clock

Many victims believe that active negotiations legally pause the statute of limitations. This assumption is entirely false.

You can negotiate a settlement right up until the day before the two-year deadline. However, if the insurance company refuses to pay, you must still file the lawsuit before the clock strikes midnight. Negotiations offer zero protection against the statute of limitations.

Why You Need to Track the Court Deadline Separately

You must separate your insurance expectations from your legal deadlines. A lawyer tracks the statute of limitations meticulously from the very first consultation.

Tracking the court deadline ensures that your legal team can draft and file the necessary lawsuit documents if the insurance company acts in bad faith. Protecting the court deadline gives you the ultimate leverage during the insurance negotiation phase.

Are There Exceptions That Can Extend or Change the Deadline

Florida law provides a few narrow exceptions that can alter the standard timeline. Courts apply these exceptions very strictly.

The Discovery Rule May Apply in Limited Cases

The “discovery rule” delays the start of the statute of limitations until the victim discovers, or reasonably should have discovered, their injury.

Florida courts apply the discovery rule frequently in medical malpractice cases. If a surgeon leaves a sponge inside a patient, the patient might not discover the error until an X-ray reveals it three years later. The deadline begins when the patient discovers the retained object.

Tolling May Apply in Certain Circumstances

Florida Statute 95.051 allows courts to “toll” or pause the deadline clock in highly specific scenarios.

The court may toll the statute of limitations if the at-fault defendant flees the state of Florida to avoid being served with a lawsuit. The court may also toll the deadline if the defendant uses a false name to hide their identity from the victim.

Fraud or Concealment May Affect the Timeline

Defendants sometimes use deliberate fraud to hide their negligence. If a property owner actively conceals evidence of a structural defect that caused a collapse, the court may intervene.

Florida law extends the filing deadline when a defendant intentionally prevents the victim from discovering the cause of their injuries. The extended timeline begins once the victim uncovers the fraudulent concealment.

Exceptions Are Narrow and Should Not Be Relied on Without Legal Advice

You cannot rely on exceptions as a backup plan for a late filing. Judges view tolling exceptions with extreme skepticism.

The defense will aggressively fight any attempt to extend the statute of limitations. You must secure legal representation immediately to ensure you meet the primary deadline, rather than gambling on a rare legal exception.

Why You Should Act Before the Deadline Gets Close

Waiting until month 23 to hire a lawyer creates a crisis for your legal claim. Successful personal injury cases require extensive preparation long before the lawsuit is filed.

Evidence Can Disappear Quickly

Attorneys need time to dispatch investigators to the accident scene. They must photograph skid marks, measure sightlines, and secure physical debris.

They also need time to subpoena security footage from nearby businesses before the digital files are deleted. If you wait a year to start your case, this critical physical evidence will vanish entirely.

Medical Records and Bills Take Time to Gather

Proving damages requires comprehensive medical documentation. Hospitals and clinics often take 30 to 60 days just to process a standard medical records request.

Your attorney needs all your surgical reports, physical therapy notes, and billing statements to calculate your total financial losses. Gathering thousands of pages of medical history takes significant administrative time.

Your Attorney Needs Time to Investigate and File Properly

Drafting a civil lawsuit requires precision. Your attorney must identify every single liable party, locate their corporate addresses, and determine their insurance coverage limits.

Rushing this process leads to errors. A lawyer needs adequate time to prepare a flawless legal complaint that withstands the defense’s initial attempts to dismiss the case.

What Should You Do After an Accident in Florida

Your actions immediately following an accident dictate the future success of your personal injury claim. Protect your health and your legal rights by following specific steps.

Get Medical Treatment Right Away

Florida law requires accident victims to seek medical care within 14 days to activate their Personal Injury Protection (PIP) benefits. Visit an emergency room or urgent care center immediately. Delaying medical care allows the insurance company to argue that your injuries resulted from a separate, unrelated event.

Report the Accident

Call 911 immediately after a traffic collision. The responding officer will create an official crash report detailing the scene, the parties involved, and any traffic citations issued. This police report serves as foundational evidence for your civil claim.

Save Evidence

Use your smartphone to document the aftermath. Take clear photos of vehicle damage, your physical injuries, and surrounding road conditions. Collect the names and phone numbers of any bystanders who witnessed the incident.

Avoid Giving Recorded Statements Without Legal Advice

Insurance adjusters will call you quickly, asking for a recorded statement. They use these recordings to extract apologies or contradictory statements. Decline the recording and instruct the adjuster to speak with your legal counsel.

Contact a Florida Personal Injury Lawyer Before the Deadline Approaches

Do not wait for the insurance company to deny your claim. Secure legal representation in the first few days following your accident. Early legal intervention prevents costly mistakes and ensures you meet all statutory filing deadlines.

How a Florida Personal Injury Lawyer Can Help Protect Your Claim

Navigating the post-accident legal system requires professional expertise. An experienced attorney takes over the administrative burden so you can focus entirely on your physical recovery.

Identify the Correct Filing Deadline

Your attorney will immediately review the date of your accident and determine the exact statute of limitations governing your case. They will lock this deadline into their case management system, ensuring the firm takes necessary legal action well before the clock expires.

Determine Whether a Special Timeline Applies

If your accident involves a government vehicle, a defective product, or medical negligence, your lawyer will identify the special procedural rules. They will draft and submit the mandatory pre-suit notices required to preserve your right to sue a municipality or hospital.

Preserve Evidence Before It Disappears

Law firms deploy private investigators to track down witnesses and secure video footage. Your attorney will send formal “spoliation letters” to defendants, legally prohibiting them from destroying critical evidence like trucking logs or commercial vehicle maintenance records.

Handle Insurance Communications

Once you hire an attorney, the insurance company can no longer contact you directly. Your lawyer will handle all negotiations, demand letters, and settlement discussions. They will force the insurer to evaluate your claim based on concrete medical evidence rather than corporate profit margins.

File a Lawsuit Before the Deadline If Necessary

If the insurance company refuses to offer a fair settlement, your attorney will draft the legal complaint and file the lawsuit in the appropriate Florida circuit court. Filing this lawsuit effectively stops the statute of limitations clock and forces the defense into formal litigation.

Talk to a Florida Personal Injury Attorney Before Time Runs Out

Do not let legal technicality destroy your right to financial recovery. The insurance company has a team of lawyers protecting their profits; you need a dedicated team protecting your future.

Free Case Review

Not sure how much time you have left to file a personal injury claim in Florida? Contact our team today for a free consultation. At Jimenez Mazzitelli Mordes, we can review your accident date, claim type, and legal options before your deadline expires. Our Miami personal injury attorneys fight aggressively for maximum compensation in car accidents, medical malpractice, and wrongful death cases.

No Fee Unless We Win

We handle all personal injury claims on a strict contingency fee basis. You pay nothing upfront, and you owe us zero attorney fees unless we successfully recover a settlement or jury verdict on your behalf. Call Jimenez Mazzitelli Mordes today to protect your claim.

Frequently Asked Questions

Did Florida change the statute of limitations for personal injury cases?

Yes. In March 2023, Florida House Bill 837 reduced the statute of limitations for general negligence claims from four years down to two years.

When exactly does the two-year deadline start?

The two-year legal clock starts running on the exact date your accident occurs.

Does filing an insurance claim pause the legal deadline?

No. Opening an insurance claim or negotiating a settlement does not stop the statute of limitations from expiring. You must file a formal lawsuit in court before the deadline passes.

What is the deadline to file a medical malpractice claim in Florida?

Medical malpractice claims generally must be filed within two years from the date the incident occurred or the date the injury was discovered. Florida also enforces a strict four-year maximum statute of repose for these claims.

How long do I have to file a wrongful death lawsuit?

Florida law dictates a two-year statute of limitations for wrongful death claims. This two-year window begins on the exact date of the victim’s death.

Can I sue a Florida city or county for my injuries?

Yes, but you face stricter deadlines. You must provide formal written notice to the government agency within three years of the incident before you can file a lawsuit.

What happens if I file my lawsuit after the two-year deadline?

The court will dismiss your case with prejudice. You will permanently lose your right to recover any financial compensation from the at-fault party.

Are there any exceptions for injured minors?

Yes. Florida law allows the statute of limitations to be tolled (paused) for up to seven years in cases involving injured children.

Do I really need a lawyer if the insurance company is offering me a settlement?

Yes. Insurance companies frequently offer lowball settlements to unrepresented victims. An attorney evaluates the true value of your medical needs and ensures the insurance company does not run out the clock on your claim.

How much does it cost to hire Jimenez Mazzitelli Mordes?

We operate on a contingency fee basis. Your initial consultation is completely free, and you pay zero attorney fees unless our firm wins your case and recovers financial compensation for you.